Is it the end of the short 1x2 put ratio as a viable tail hedge?

As usual, we relied heavily on the Allasso backtesting and analytics engine for this.

Short 1x2 put ratio spreads are, by now, widely known hedges against an equity market sell off.

We mapped out a hedge fairly far down the October put skew in Allasso Copilot (see Figure 1).

In particular, we sold some 10 delta puts on S&P E minis and bought 2X as many 5 delta puts with the same maturity.

We’re approximately delta neutral and a mild (though not insignificant) payer of premium.

The trade provides significant downside coverage as we cross the lower 5175 strike. It also provides some edge if we believe that the odds of a move down to 5175 is higher than the market odds of 1 in 20.

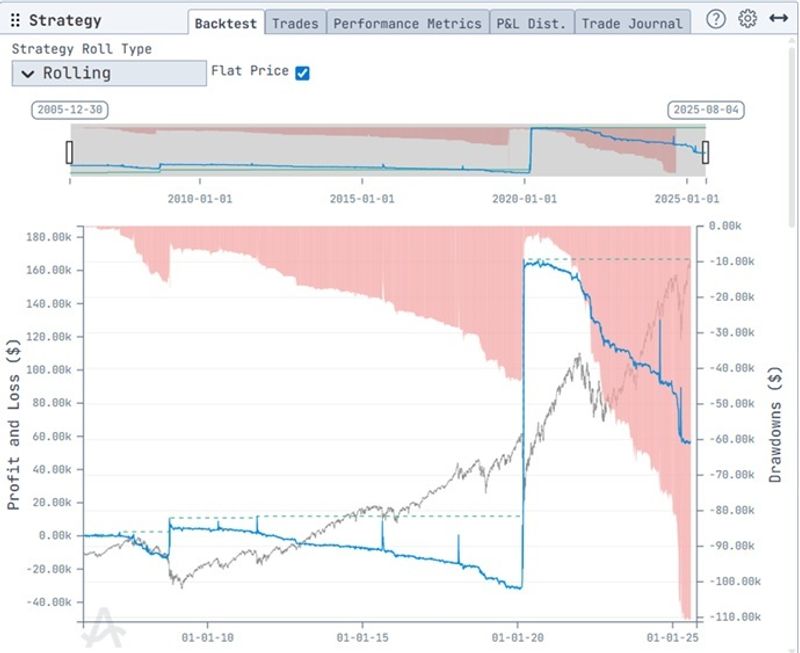

The long-term backtest is extremely attractive (Figure 2), especially if we are quick to take profits during pre-2020 profit spikes. Historically, this was a fine tail hedge.

However, post-Covid, we see far more decay in the strategy. The 5 delta skew seems relatively rich nowadays.

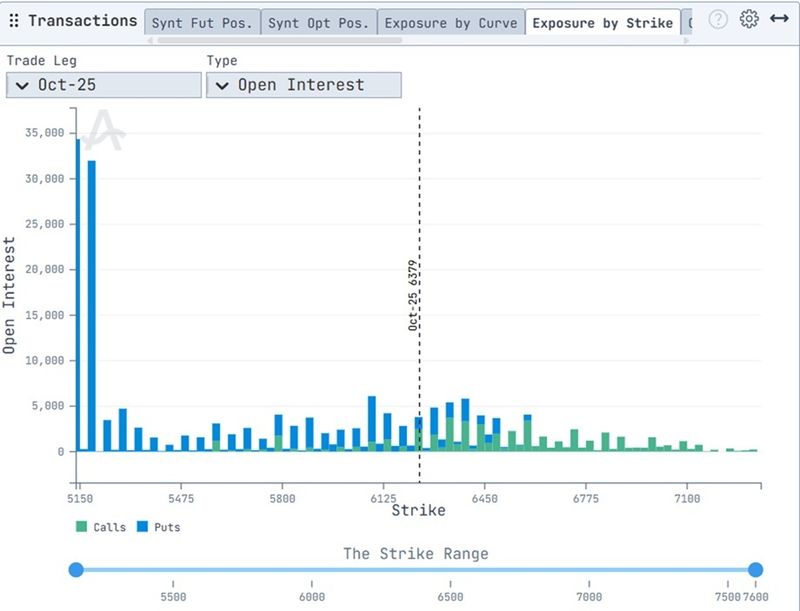

Open interest has loaded on the far if not extreme downside (Figure 3). Clearly, some market participants haven’t forgotten March 2020, along with the potential for more radical political uncertainty.

This is true even in delta-adjusted terms (Figure 4).

Does this spell the end of the short 1x2 put ratio as a viable tail hedge?

Not necessarily, a strategy that doesn’t backtest well can still be successful in practice, given selective entry points, efficient delta hedging and so on.

Nonetheless, we would hope to see a reduction in open interest along the farther reaches of the put skew before implementing the strategy as an “all weather” hedge.

As ever, this is not to be taken as trading advice.