Presenting a case for “owning” the US soybean crop using futures options, and testing its historical performance over time

Let’s focus on agricultural options using the Allasso engine.

Check out this local article that came across my desk recently.

Shawn Hackett and others see potential upside in beans, given low acreage numbers and potential demand for soybean oil as a cleaner alternative to standard diesel.

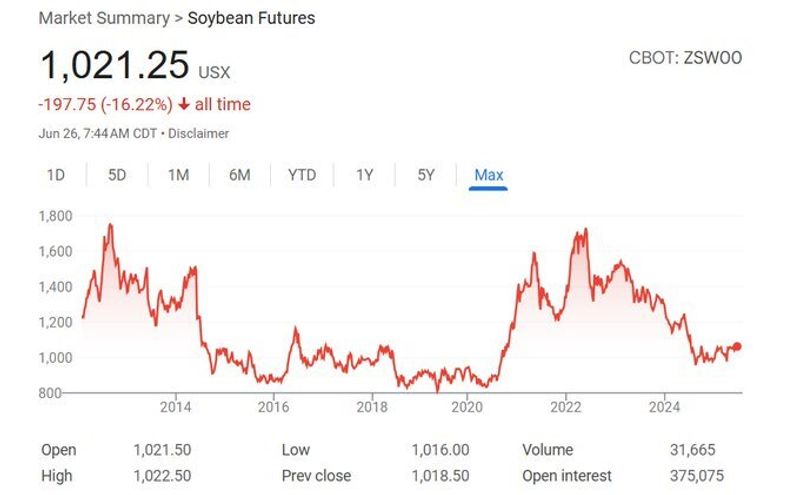

Low acreage typically correlates to low prices, with a lag. Figure 1, below, characterises a cheap commodity that (at least for now) is not trending down so badly that you have to catch the falling knife.

Here's a market that surges and declines sharply: you don't want to be exposed to open ended risk. A simple call spread can be enough to express a bullish view.

Figure 2 tracks the relative performance of a 50/30 delta call spread, rolled with 30 days to go, over time.

While the call spread (in blue) does have negative bleed, price rallies have been sharp enough and the call skew expensive enough for the trade to have legs. The distance between the strikes increases on the way up, assuming a steepening skew, which increases upside capture.

As always, not to be taken as trading advice.