Searching for unusual options flow across global markets

Let’s take a cue from Unusual Whales, with help from the Allasso engine.

Whales scans for unusual options flow predominantly in US equity options, but we can extend the idea to other markets, such as short-term interest rates.

The overarching idea is that, when open interest increases sharply at certain strikes, a large new position is being established. Maybe the options market knows something, but at the very least, this mega trade has the potential to distort markets.

A workaround for rates and commodities

While Unusual Whales offers fairly comprehensive coverage of listed options on US securities, we need a workaround for rates and commodities. The recent mega flows into SOFR 3-month September futures options catches the attention.

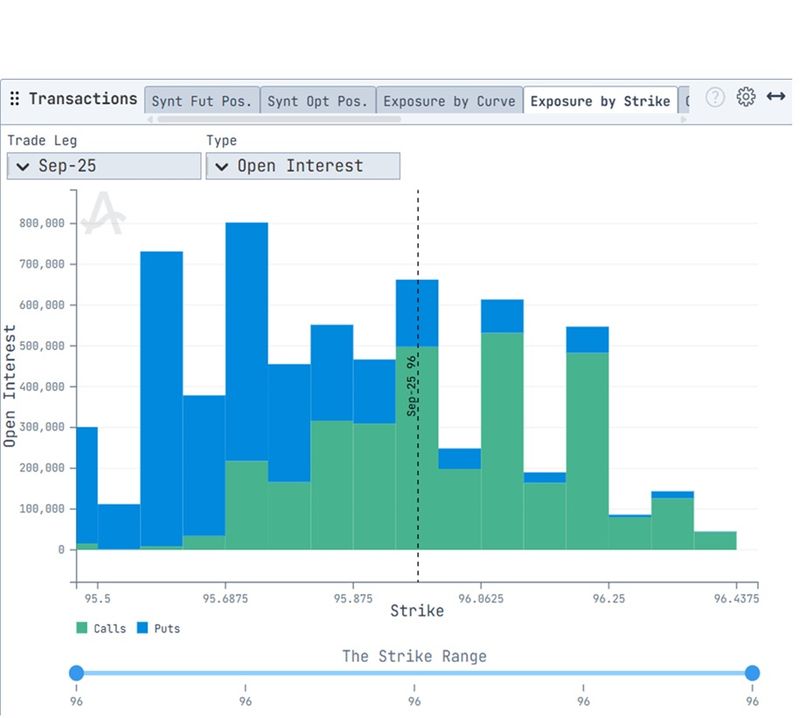

In Figure 1, see a time series of the underlying futures, taken directly from the CME website.

In Figures 2 and 3, below, using Allasso Copilot, we see a significant increase in open interest for the 96.125 and 96.25 strikes expiring on 12 September. The bar charts below have been taken from 4 and 13 August, respectively.

Open interest picked up substantially at both strikes (see Figure 4 and 5, below), indicating a call spread going through the market. Skew flattening in the 96.10 to 96.2 area suggests that the orders were a resounding BUY. Dealers raised their quotes for the call spread, locally compressing the skew.

Even the 96.125 strike is quite far out of the money, as the Fed funds market is currently pricing a 25 basis point cut in September. A 50 basis point Bessent-influenced cut pushes us slightly beyond the 96.125 strike at maturity. Not bad, but not ideal.

However, if September futures start drifting toward 96.125, dealers may have to buy futures as their short deltas increase, with the call spread acting like a giant magnet.

The mega buyers will benefit from feedback, if they are able to quietly manage their position.

As ever, this should not be construed as investment advice.